Free insurance – Does it benefit a new recruit into HM Forces

The provision of Free Insurance to new recruits at all levels has been an established practice within most services in HM Forces for quite a few years now. The overall aim of insurance companies providing cover for a new entrants Military Kit and Personal Possessions, in typically their first time away from home, not having needed insurance previously, is I believe, totally justified.

In fact over the last few years, Free Insurance periods on offer have risen from an initial 3 months to what is now an established norm of around 12 months free cover in most establishments, as military brokers compete for each recruits business.

Over the years practices have changed too. These have ranged from allocated companies delivering briefs to allocated groups, to group presentations by all insurance companies to the boys and girls in lecture theatres and also Fresher Fayre type days resembling Student enrolment days in Civvy Street.

This competition has been great for the military, driving up free cover periods, as referred to earlier. Although the ever increasing benefits included in policies, in a bid to win customers can also cause confusion due to the amount of information being delivered, in some cases, the need to make instant decisions plus application form completion in limited time periods means that nowadays many choose not to accept the offer and “self-insure”.

Even more worrying, is the fact that Free Insurance may no longer be worth it, even in the short term!! How can something that is Free not be worth it?

Well everything is rosy, providing the post Free period prices on offer are low enough! However that does not appear to be the case anymore as over the past few years, as with the rest of the Military Kit market, prices have crept up and up, due to a number of reasons, one of the main ones being the levels of cover being offered in many cases being far too much for the customer requirements.

Existing providers will continue to adhere to the status quo until a provider bucks the trend!!

So if a company decides NOT to “play” in the Free Insurance market and launch Kit & Personal Possessions products, that are sensibly priced, for the long term, with a cost that negates Free period terms – the Free Insurance model will start to buckle under pressure very quickly. Take the example above

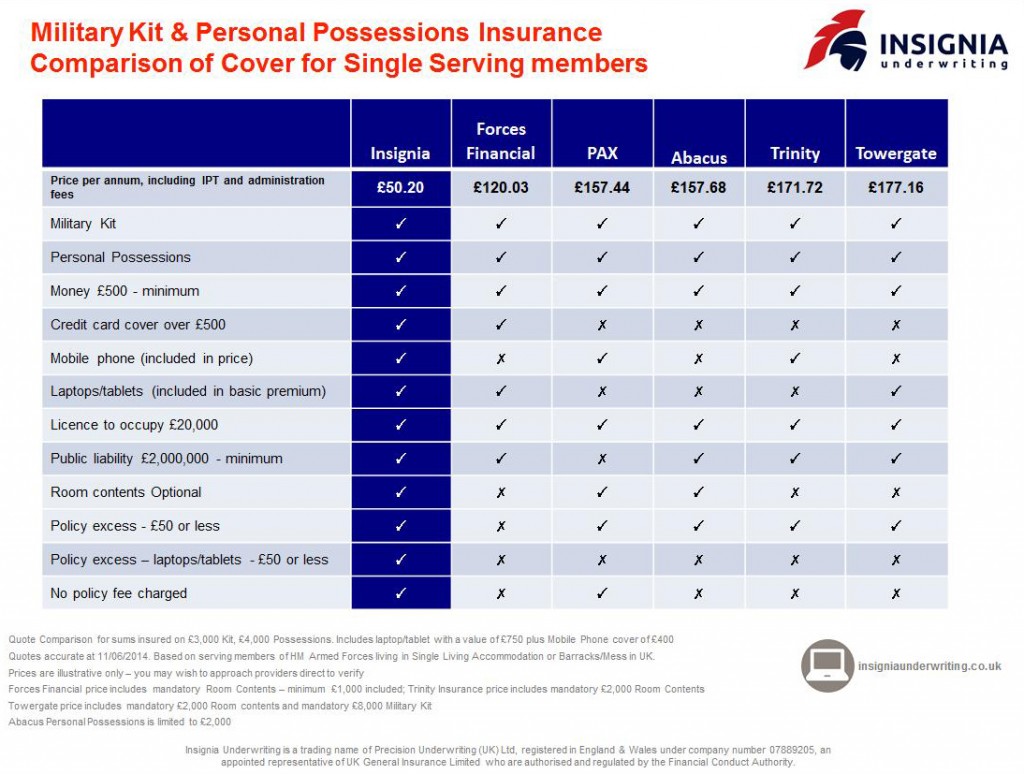

A typical recruit with one year’s Free Insurance at Phase 1, committing to a further 12 months paid insurance with their chosen Free Cover provider would still pay at the minimum almost £20 MORE over the two year period, than choosing to insure and pay from Day 1 with a reasonable priced company.

Why the low prices? It puts much needed value back into the market and Phase 1 Units and the New Recruits will only benefit from military brokers needing to reassess their offers to compete – The customer will be the winner. It can also help save the potential customers confusion of having to make an instant decision in a limited time period. The ability to choose and buy on line gives more time for an informed decision, and knowing full well it’s not going to cost the earth for the protection he or she needs it can more importantly can overcome potential a lack of insurance during and even after the free period

Free Insurance is a superb benefit BUT is it all it’s cut out to be?